Term Life vs. Whole Life Insurance: A Clear Comparison

- Alex Ewert

- Jan 7

- 2 min read

By Alexander Ewert Published on January 7, 2026

When choosing life insurance, the two most common options are term life and whole life (a type of permanent insurance). Term life is like renting coverage for a specific period, while whole life is like owning it for life with added investment features. The right choice depends on your needs, budget, and financial goals. Here's a straightforward breakdown to help you decide.

Key Differences at a Glance

Here's a side-by-side comparison:

Feature | Term Life Insurance | Whole Life Insurance |

Coverage Duration | Fixed term (e.g., 10, 20, or 30 years) | Lifelong, as long as premiums are paid |

Premiums | Lower and fixed for the term | Higher and fixed for life |

Cash Value | None | Builds over time (grows tax-deferred) |

Death Benefit | Paid if death occurs during term | Guaranteed payout whenever death occurs |

Best For | Temporary needs (e.g., mortgage, kids' education) | Long-term security and wealth building |

Term Life Insurance: Simple and Affordable Protection

Term life provides pure death benefit coverage for a set period. If you pass away during the term, your beneficiaries get the payout. If you outlive it, the policy expires with no value.

Term vs Permanent Life Insurance

Pros:

Much cheaper premiums—often 8-10 times less than whole life for the same coverage.

Allows higher coverage amounts for the same budget.

Simple and straightforward—no investment complexity.

Cons:

No payout if you outlive the term (most policies expire without benefit).

Premiums can skyrocket if renewed after the term.

No cash value or savings component.

In 2026, term life remains popular for young families needing high coverage on a budget.

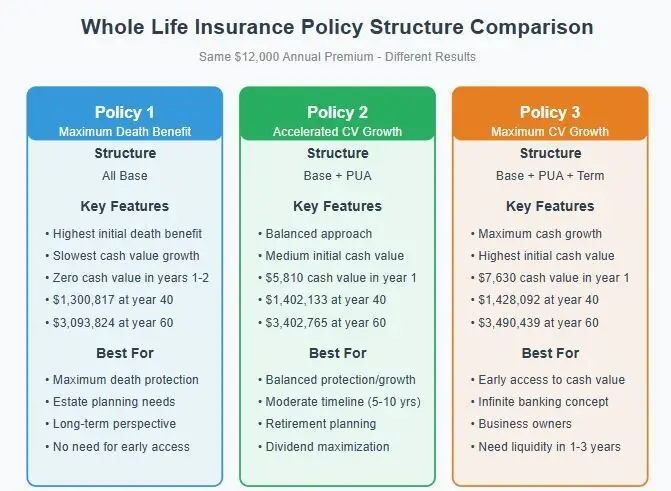

Whole Life Insurance: Lifelong Coverage with Savings

Whole life is permanent insurance that lasts your entire life and includes a cash value component that grows over time (like a forced savings account). You can borrow against or withdraw from it.

Pros:

Guaranteed death benefit no matter when you die.

Cash value grows tax-deferred and can be used for loans, retirement, etc.

Fixed premiums that never increase.

Potential dividends from mutual insurers.

Cons:

Significantly more expensive (e.g., $400–$500/month vs. $30–$50/month for similar coverage in term).

Lower initial death benefit for the same premium.

Opportunity cost: Many experts say "buy term and invest the difference" yields better returns elsewhere.

Cost Comparison (2026 Estimates)

For a healthy 35-year-old non-smoker seeking $1 million coverage:

Term (30-year): Around $50–$100/month.

Whole Life: $500–$800/month or more.

Whole life can cost 8–15 times more, but part of that premium builds cash value.

Which Should You Choose?

Choose Term if you need coverage for a specific timeframe (e.g., until kids are grown or mortgage paid) and want to maximize protection while keeping costs low. Invest the premium savings in retirement accounts for potentially higher returns.

Choose Whole if you want guaranteed lifelong coverage, estate planning benefits, or a conservative savings vehicle.

Many financial experts lean toward term for most people, as it's more cost-effective. However, whole life suits high-net-worth individuals or those seeking forced savings.

This is general info—rates vary by age, health, and insurer. Get quotes and consult a licensed advisor for your situation.

What’s your take? Planning to go with term or whole? Drop a comment!

Alexander Ewert is a personal finance writer in California, sharing practical tips on insurance and money management.

Comments